世界のカルシニューリン阻害剤市場規模(2025~2034年):製品別(ブランド、ジェネリック)、用量別、疾患別

| 本レポートは、特定の市場における研究調査の方法論と範囲を詳述しています。第1章では市場の範囲と定義、調査デザイン、データ収集方法、基準年の算出、予測モデル、一次調査の手法について説明しています。調査は、主に一次情報源とデータマイニングを基に行われました。 第2章では、産業の全体像をエグゼクティブサマリーとしてまとめています。第3章では、業界のエコシステム分析や成長促進要因、課題について詳しく述べており、特に臓器移植手術の増加や自己免疫疾患の有病率上昇が成長に寄与していることが指摘されています。また、免疫抑制剤の研究開発活動の増加と、それに伴う副作用や代替治療の利用可能性についても言及されています。 第4章では、2024年の競争環境を分析し、企業のシェアや競合分析を行っています。主要市場プレーヤーの競合状況や戦略についても触れています。 第5章から第8章では、2021年から2034年にかけての市場推定と予測が示されており、製品別、投与量別、疾患別、地域別のデータが提供されています。特に、タクロリムスやシクロスポリンなどのブランド製品やジェネリックの市場動向が詳しく分析されています。地域別のセクションでは、北米、ヨーロッパ、アジア太平洋、ラテンアメリカ、中東・アフリカの各地域における市場の動向をまとめています。 最後に第9章では、主要企業のプロフィールが紹介されています。abbvie、astellas、Aurinia、Biocon、Dr. Reddy’s、Glenmark、LUPIN、Novartis、Roche、VIATRISなどの企業が含まれており、それぞれの会社の戦略や市場におけるポジションについても言及されています。全体として、このレポートは市場動向、競争環境、企業戦略に関する包括的な情報を提供しています。 |

*** 本調査レポートに関するお問い合わせ ***

Calcineurin Inhibitors Market Size

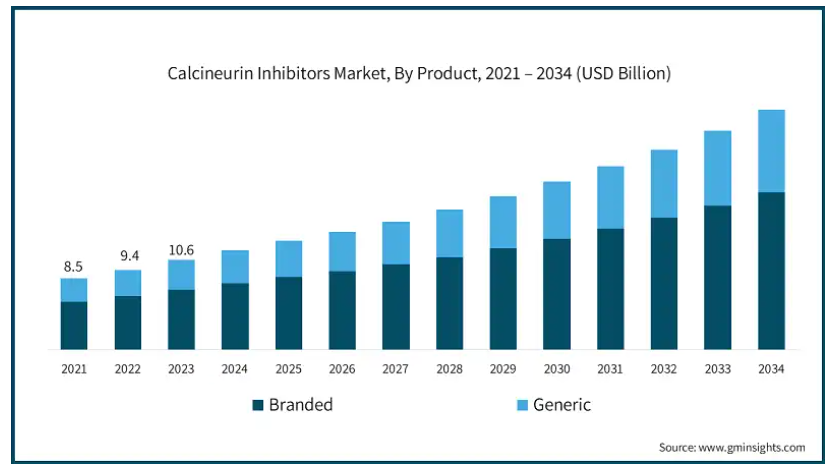

The global calcineurin inhibitors market size was valued at USD 11.7 billion in 2024 and is expected to exhibit growth at a CAGR of 9.2% from 2025 to 2034 period. The market growth is attributed to the increasing number of organ transplant procedures and the rising prevalence of autoimmune diseases, leading to growing adoption of these solutions.

Calcineurin inhibitors, such as cyclosporine and tacrolimus, are indispensable in transplant medicine. They work by suppressing the immune system to prevent rejection of transplanted organs. With the rising volume of transplants, including kidney, liver, heart, and lung procedures, the demand for these organ transplant rejection medication products continues to grow.

Additionally, global initiatives to improve organ donation rates, coupled with advancements in organ preservation and surgical techniques, have significantly increased the number of successful transplant procedures. This growth directly fuels the need for calcineurin inhibitors to manage post-operative care and ensure long-term transplant success.

Calcineurin inhibitors are a class of immunosuppressive drugs that work by inhibiting the activity of calcineurin, a protein phosphatase critical for the activation of T-cells in the immune system. By suppressing T-cell activation, these drugs reduce immune responses and inflammation, which makes them especially useful in treating conditions where the immune system is overly active.

Calcineurin Inhibitors Market Trends

The surge in immunosuppressive research and development (R&D) activities is a significant growth driver for the market. Ongoing advancements in immunosuppressive therapies, supported by substantial R&D investments, are driving innovation and expanding the clinical applications of calcineurin inhibitors.

Continuous R&D efforts in immunosuppressive drugs are enhancing the safety, efficacy, and tolerability of calcineurin inhibitors. Researchers are focusing on minimizing side effects, such as nephrotoxicity while improving their ability to target specific immune pathways. These advancements make calcineurin inhibitors more appealing for long-term use in transplant and autoimmune patients.

Additionally, pharmaceutical companies are increasingly investing in R&D to develop next-generation immunosuppressive drugs. With calcineurin inhibitors already established as a cornerstone in transplant medicine, companies aim to refine these drugs or develop combination therapies to address broader patient needs. Such efforts are fueling growth in the market.

Calcineurin inhibitors Market Analysis

Based on product, the market is segmented as branded and generic. The branded segment is expected to drive business growth and expand at a CAGR of 9%, reaching over USD 18.6 billion by 2034.

Branded calcineurin inhibitors, such as Prograf (tacrolimus) and Neoral (cyclosporine), are widely recognized for their proven clinical efficacy and safety profiles. Physicians often prefer prescribing branded drugs due to their consistent performance and extensive clinical trial backing, ensuring reliable patient outcomes.

Branded calcineurin inhibitors adhere to rigorous manufacturing and quality control standards, providing assurance of product reliability and safety. This factor plays a crucial role in the treatment of critical conditions like organ transplantation and autoimmune diseases, where precision in drug formulation is vital.

Based on dosage, the calcineurin inhibitors market is classified into tablets and capsules, ointments, injections, and other dosage forms. The tablets and capsules segment dominated the market with a revenue share of 41.8% in 2024.

Tablets and capsules are easy to administer, making them ideal for patients who require regular dosing of calcineurin inhibitors. Their non-invasive nature and portability ensure high adherence to prescribed treatment regimens, particularly for chronic conditions like organ transplantation and autoimmune diseases.

Patients undergoing organ transplants or managing autoimmune disorders often require lifelong or extended use of calcineurin inhibitors. Tablets and capsules, with their extended shelf life and ease of storage, are better suited for prolonged treatments compared to other forms like injectables.

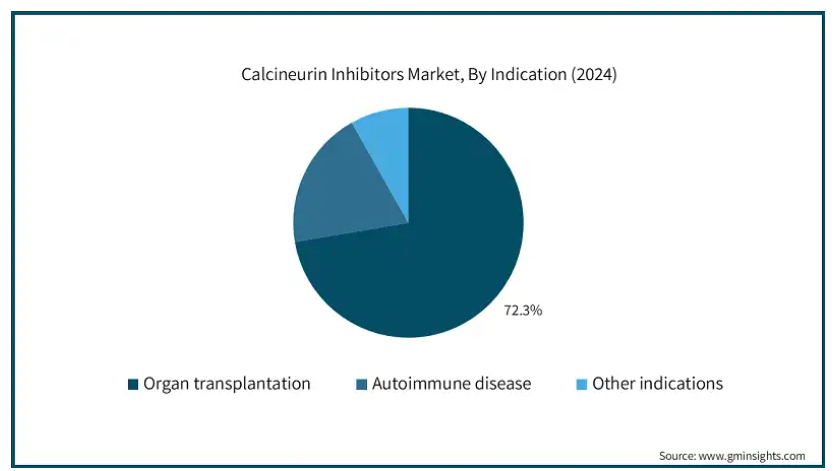

Based on indication, the calcineurin inhibitors market is classified into organ transplantation, autoimmune disease, and other indications. The organ transplantation segment dominated the market in 2024 and is anticipated to reach USD 20.2 billion by the end of the forecast period.

Calcineurin inhibitors are crucial in post-transplantation regimens, as they effectively suppress the immune system to prevent the body from rejecting transplanted organs. Their efficacy and reliability make them the first-line choice in immunosuppressive protocols, solidifying their dominance in this segment.

The rising prevalence of end-stage organ failure due to chronic conditions like diabetes, cardiovascular diseases, and liver cirrhosis has led to a surge in organ transplantation rates. This growth directly fuels the demand for calcineurin inhibitors to ensure transplant success and longevity, thereby fueling the market growth.

The U.S. calcineurin inhibitors market accounted for USD 4.3 billion in 2024 and is anticipated to grow at a CAGR of 8.4% between 2025 to 2034 period.

Leading transplant centers, well-established reimbursement policies, and a strong focus on research and development support the market growth in the region.

Additionally, the U.S. has a large population with chronic diseases such as diabetes and hypertension, which often result in end-stage organ failure, further increasing the demand for calcineurin inhibitors.

France calcineurin inhibitors market is projected to grow remarkably in the coming years.

The country is recognized for its efficient organ transplant networks and high success rates, bolstered by government initiatives to promote organ donation.

French pharmaceutical companies also play a crucial role in the production and distribution of calcineurin inhibitors, ensuring accessibility and sustained market growth.

Japan holds a dominant position in the Asia Pacific calcineurin inhibitors market.

The country’s advanced medical technology, coupled with strong government support for organ transplantation, underpins the demand for calcineurin inhibitors.

Additionally, Japan’s focus on research and innovation in immunosuppressive therapies contributes to the growth of the market.

Calcineurin Inhibitors Market Share

Several key players in the market are making strides in product innovation and strategic partnerships to maintain market leadership. Companies are investing heavily in R&D to develop advanced calcineurin inhibitors with enhanced features such as the development of personalized medicine, the introduction of novel drug delivery systems, and the expansion of applications beyond transplantation.

Additionally, partnerships with healthcare providers are being forged to improve product accessibility in emerging markets. Regulatory compliance and adherence to international quality standards are crucial aspects of the strategies employed by these companies to cater to a global market. These developments are helping companies meet the increasing demand for safe and efficient calcineurin inhibitors.

Calcineurin Inhibitors Market Companies

Prominent players operating in the calcineurin inhibitors industry include:

abbvie

astellas

Aurinia

Biocon

Dr. Reddy’s

Glenmark

LUPIN

Novartis

Roche

VIATRIS

Calcineurin Inhibitors Industry News:

In July 2021, Astellas Pharma Inc. announced that the U.S. Food and Drug Administration (FDA) has expanded the indication for PROGRAF (tacrolimus) to include the prevention of organ rejection in adult and pediatric lung transplant recipients. PROGRAF, initially approved for liver transplants nearly three decades ago, is now indicated for liver, kidney, heart, and lung transplants, making it a versatile option for preventing organ rejection across multiple transplant types.

The calcineurin inhibitors market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million from 2021 – 2034 for the following segments:

Market, By Product

Branded

Tacrolimus

Cyclosporine

Other branded products

Generic

Tacrolimus

Cyclosporine

Other generic products

Market, By Dosage

Tablets and capsules

Ointments

Injections

Other dosage forms

Market, By Indication

Organ transplantation

Autoimmune disease

Other indications

The above information is provided for the following regions and countries:

North America

U.S.

Canada

Europe

Germany

UK

France

Spain

Italy

Netherlands

Asia Pacific

China

Japan

India

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

Middle East and Africa

South Africa

Saudi Arabia

UAE

カルシニューリン阻害剤の市場規模

カルシニューリン阻害剤の世界市場規模は、2024年に117億米ドルと評価され、2025年から2034年にかけてCAGR 9.2%で成長すると予測されています。市場成長の背景には、臓器移植手術の増加や自己免疫疾患の有病率の上昇があり、これらのソリューションの採用が拡大しています。

シクロスポリンやタクロリムスなどのカルシニューリン阻害剤は、移植医療に不可欠な薬剤です。シクロスポリンやタクロリムスなどのカルシニューリン阻害剤は、移植医療に欠かせない薬剤です。腎臓、肝臓、心臓、肺などの移植件数の増加に伴い、これらの臓器移植拒絶反応治療薬の需要は増加の一途をたどっています。

さらに、臓器提供率を向上させるための世界的な取り組みと、臓器保存や手術技術の進歩が相まって、移植手術の成功件数が大幅に増加しています。この成長は、術後のケアを管理し、長期的な移植の成功を確実にするためのカルシニューリン阻害剤の必要性を直接後押ししています。

カルシニューリン阻害剤は、免疫系におけるT細胞の活性化に重要なタンパク質リン酸化酵素であるカルシニューリンの活性を阻害することによって作用する免疫抑制剤の一種です。T細胞の活性化を抑制することにより、これらの薬剤は免疫反応と炎症を抑制し、免疫系が過剰に活性化している病態の治療に特に有用です。

カルシニューリン阻害剤の市場動向

免疫抑制剤の研究開発(R&D)活動の急増は、市場の大きな成長ドライバーです。多額の研究開発投資に支えられた免疫抑制療法の継続的な進歩が、技術革新を促進し、カルシニューリン阻害剤の臨床応用を拡大しています。

免疫抑制剤の継続的な研究開発努力により、カルシニューリン阻害剤の安全性、有効性、忍容性が向上しています。研究者たちは、特定の免疫経路を標的とする能力を向上させる一方で、腎毒性などの副作用を最小限に抑えることに注力しています。このような進歩により、カルシニューリン阻害薬は移植患者や自己免疫患者における長期的な使用にとってより魅力的なものとなっています。

さらに、製薬会社は次世代の免疫抑制剤を開発するための研究開発への投資を増やしています。カルシニューリン阻害剤はすでに移植医療の基礎として確立されており、各社はこれらの薬剤を改良したり、より幅広い患者のニーズに対応するための併用療法を開発したりすることを目指しています。こうした取り組みが市場の成長を後押ししています。

カルシニューリン阻害薬市場の分析

カルシニューリン阻害薬市場は、製品によってブランド品とジェネリック医薬品に区分されます。ブランド品セグメントは事業の成長を牽引し、年平均成長率9%で拡大し、2034年には186億米ドル以上に達する見込み。

プログラフ(タクロリムス)やネオーラル(シクロスポリン)などのカルシニューリン阻害剤のブランドは、その臨床効果と安全性プロファイルが証明されていることから広く認知されています。一貫した性能と広範な臨床試験の裏付けにより、信頼性の高い患者の転帰が保証されるため、医師はしばしばブランド薬の処方を好みます。

ブランド品のカルシニューリン阻害剤は厳格な製造・品質管理基準を遵守しており、製品の信頼性と安全性が保証されています。この要素は、臓器移植や自己免疫疾患のような、製剤の精度が極めて重要な疾患の治療において重要な役割を果たしています。

カルシニューリン阻害剤市場は、剤形によって錠剤・カプセル剤、軟膏剤、注射剤、その他の剤形に分類されます。2024年の売上高シェアは錠剤・カプセル剤が41.8%で市場を支配。

錠剤とカプセルは投与が容易なため、カルシニューリン阻害剤の定期的な投与が必要な患者に最適。非侵襲的で携帯性に優れているため、特に臓器移植や自己免疫疾患などの慢性疾患において、処方された治療レジメンへの高いアドヒアランスが保証されます。

臓器移植を受ける患者や自己免疫疾患を管理する患者は、しばしばカルシニューリン阻害薬を終生あるいは長期にわたって使用する必要があります。錠剤やカプセルは保存期間が長く、保管が容易であるため、注射剤のような他の剤形と比較して長期の治療に適しています。

適応症別では、カルシニューリン阻害薬市場は臓器移植、自己免疫疾患、その他の適応症に分類されます。2024年には臓器移植分野が市場を支配し、予測期間終了時には202億米ドルに達すると予測されています。

カルシニューリン阻害剤は、免疫系を効果的に抑制して移植臓器の拒絶反応を防ぐため、移植後のレジメンにおいて極めて重要です。その有効性と信頼性により、免疫抑制プロトコールにおける第一選択薬となっており、このセグメントにおける優位性を確固たるものにしています。

糖尿病、心血管疾患、肝硬変などの慢性疾患による末期臓器不全の有病率の上昇は、臓器移植率の急増につながっています。この成長は、移植の成功と長寿を確実にするためのカルシニューリン阻害剤の需要を直接後押しし、市場の成長に拍車をかけています。

アメリカのカルシニューリン阻害剤市場は2024年に43億米ドルを占め、2025年から2034年の間に年平均成長率8.4%で成長すると予測されています。

主要な移植センター、確立された償還政策、研究開発への強い注力などが、この地域の市場成長を支えています。

さらに、アメリカは糖尿病や高血圧などの慢性疾患を抱える人口が多く、しばしば末期臓器不全を引き起こすため、カルシニューリン阻害薬の需要がさらに高まっています。

フランスのカルシニューリン阻害剤市場は、今後数年間で著しく成長すると予測されています。

同国は、臓器提供を促進する政府の取り組みにより、効率的な臓器移植ネットワークと高い成功率が認められています。

また、フランスの製薬会社はカルシニューリン阻害剤の生産と流通において重要な役割を果たしており、市場へのアクセス性と持続的な成長を保証しています。

日本は、アジア太平洋地域のカルシニューリン阻害薬市場において支配的な地位を占めています。

高度な医療技術と臓器移植に対する政府の強力な支援が、カルシニューリン阻害剤の需要を支えています。

さらに、日本は免疫抑制療法の研究と技術革新に注力していることも、市場の成長に寄与しています。

カルシニューリン阻害薬市場シェア

カルシニューリン阻害薬市場の主要プレーヤー数社は、製品革新や戦略的提携に邁進し、市場でのリーダーシップを維持しています。企業は研究開発に多額の投資を行い、個別化医療の開発、新規ドラッグデリバリーシステムの導入、移植以外の用途の拡大などの機能を強化した先進的なカルシニューリン阻害剤を開発しています。

さらに、新興市場における製品の入手しやすさを向上させるため、医療提供者とのパートナーシップも構築されています。規制順守と国際的な品質基準の遵守は、グローバル市場に対応するためにこれらの企業が採用する戦略の重要な側面です。このような開発は、安全で効率的なカルシニューリン阻害剤に対する需要の高まりに対応する上で、各社を支援しています。

カルシニューリン阻害剤市場の企業

カルシニューリン阻害剤業界で事業を展開している主な企業は以下の通り:

abbvie

astellas

Aurinia

Biocon

Dr. Reddy’s

Glenmark

LUPIN

Novartis

Roche

VIATRIS

カルシニューリン阻害剤 業界ニュース

2021年7月、アステラス製薬株式会社は、アメリカ食品医薬品局(FDA)がプログラフ(タクロリムス)の適応を拡大し、成人および小児の肺移植レシピエントにおける臓器拒絶反応の予防を追加したと発表しました。プログラフは、約30年前に肝移植の適応で承認されましたが、現在では肝移植、腎移植、心臓移植、肺移植の適応となっており、複数の移植型にまたがる臓器拒絶反応を予防する汎用性の高い選択肢となっています。

この調査レポートは、カルシニューリン阻害剤市場を詳細に調査し、2021年~2034年の市場規模(百万米ドル)を予測しています:

市場, 製品別

ブランド別

タクロリムス

シクロスポリン

その他のブランド製品

ジェネリック

タクロリムス

シクロスポリン

その他のジェネリック医薬品

用量別市場

錠剤およびカプセル

軟膏剤

注射剤

その他の剤形

疾患別市場

臓器移植

自己免疫疾患

疾患別

上記の情報は、以下の地域および国について提供されています:

北米

アメリカ

カナダ

ヨーロッパ

ドイツ

英国

フランス

スペイン

イタリア

オランダ

アジア太平洋

中国

日本

インド

オーストラリア

韓国

ラテンアメリカ

ブラジル

メキシコ

アルゼンチン

中東・アフリカ

南アフリカ

サウジアラビア

アラブ首長国連邦

第1章 方法論と範囲

1.1 市場範囲と定義

1.2 調査デザイン

1.2.1 調査アプローチ

1.2.2 データ収集方法

1.3 ベースとなる推定と計算

1.3.1 基準年の算出

1.3.2 市場推計の主要トレンド

1.4 予測モデル

1.5 一次調査と検証

1.5.1 一次情報源

1.5.2 データマイニングソース

第2章 エグゼクティブサマリー

2.1 産業3600の概要

第3章 業界インサイト

3.1 業界エコシステム分析

3.2 業界の影響力

3.2.1 成長促進要因

3.2.1.1 臓器移植手術件数の増加

3.2.1.2 自己免疫疾患の有病率の上昇

3.2.1.3 免疫抑制剤の研究開発活動の急増

3.2.2 業界の落とし穴と課題

3.2.2.1 副作用と代替治療の利用可能性

3.3 成長可能性分析

3.4 薬事規制

3.5 技術の展望

3.6 保険償還シナリオ

3.7 パイプライン分析

3.8 ポーター分析

3.9 PESTEL分析

3.10 将来の市場動向

第4章 競争環境(2024年

4.1 はじめに

4.2 企業マトリックス分析

4.3 企業シェア分析

4.4 主要市場プレーヤーの競合分析

4.5 競合のポジショニングマトリックス

4.6 戦略ダッシュボード

第5章 2021─2034年製品別市場推定・予測(単位:百万ドル)

5.1 主要トレンド

5.2 ブランド

5.2.1 タクロリムス

5.2.2 シクロスポリン

5.2.3 その他のブランド製品

5.3 ジェネリック

5.3.1 タクロリムス

5.3.2 シクロスポリン

5.3.3 その他のジェネリック医薬品

第6章 投与量別市場予測:2021〜2034年(Mnドル)

6.1 主要トレンド

6.2 錠剤およびカプセル剤

6.3 軟膏剤

6.4 注射剤

6.5 その他の剤形

第7章 2021─2034年疾患別市場予測(単位:Mnドル)

7.1 主要トレンド

7.2 臓器移植

7.3 自己免疫疾患

7.4 その他の疾患別

第8章 2021年〜2034年地域別市場予測・予測($ Mn)

8.1 主要動向

8.2 北米

8.2.1 アメリカ

8.2.2 カナダ

8.3 ヨーロッパ

8.3.1 ドイツ

8.3.2 イギリス

8.3.3 フランス

8.3.4 スペイン

8.3.5 イタリア

8.3.6 オランダ

8.4 アジア太平洋

8.4.1 中国

8.4.2 日本

8.4.3 インド

8.4.4 オーストラリア

8.4.5 韓国

8.5 ラテンアメリカ

8.5.1 ブラジル

8.5.2 メキシコ

8.5.3 アルゼンチン

8.6 中東・アフリカ

8.6.1 南アフリカ

8.6.2 サウジアラビア

8.6.3 アラブ首長国連邦

第9章 企業プロフィール

9.1 abbvie

9.2 astellas

9.3 Aurinia

9.4 Biocon

9.5 Dr. Reddy’s

9.6 Glenmark

9.7 LUPIN

9.8 Novartis

9.9 Roche

9.10 VIATRIS

*** 本調査レポートに関するお問い合わせ ***